A hailstorm can move through New Braunfels in a matter of minutes, yet the damage it leaves behind can create problems for months or even years. That’s why receiving a denial letter after filing a claim can feel like a second storm hitting your property. If you’re searching for What to Do If Your Hail Claim Was Denied in New Braunfels, TX, you’re likely dealing with frustration, uncertainty, and plenty of questions. The good news? A denied claim does not always mean the process is over.

Many homeowners assume the insurance company has the final word. In reality, claim denials are often challenged successfully when additional evidence, inspections, and documentation are presented. The key is understanding why the denial occurred and knowing the steps available to move forward. Whether your insurer claims there was no hail damage, argues that your roof problems stem from age-related wear, or believes the damage falls below your deductible, there are practical actions you can take right now. Let’s start with understanding the denial itself.

Understanding Why Hail Claims Get Denied

Before you can challenge a denial, you need to understand exactly what caused it. Insurance companies deny hail claims for several reasons. Some denials may be supported by the available evidence. Others may result from incomplete inspections, conflicting opinions, or missing documentation.

Common Reasons Hail Claims Are Denied

| Reason for Denial | What It Means |

| Wear and tear | Damage is attributed to aging materials rather than hail |

| Pre-existing damage | The insurer believes damage existed before the storm |

| Lack of evidence | Insufficient proof links damage to a specific hail event |

| Late reporting | The claim was reported long after the storm occurred |

| Policy exclusions | Certain damage types may not be covered |

| Below deductible | Repair costs are estimated below the deductible threshold |

Understanding which category applies to your situation is critical. A homeowner challenging a wear-and-tear determination will need different evidence than someone disputing a coverage exclusion.

Full Denial vs. Partial Denial

Not every denial is absolute. Some homeowners receive a complete denial with no payment whatsoever. Others receive what is effectively a partial denial. For example, an insurer may approve repairs to gutters and downspouts while denying roof replacement. They may agree hail occurred but disagree about the extent of the damage. That distinction matters because your strategy may change depending on the circumstances.

Why Hail Damage Is Frequently Disputed

Hail claims are unique. Unlike a tree crashing through a roof, hail damage is not always obvious. Two inspectors can examine the same property and arrive at completely different conclusions. One may identify widespread functional damage. Another may conclude the impacts are cosmetic.

This is particularly common with:

- Asphalt shingles

- Metal roofing systems

- Concrete tiles

- Clay tiles

- Composite roofing products

Small differences in interpretation can have a major impact on claim outcomes. That is why evidence matters far more than opinions.

Read the Denial Letter Before Doing Anything Else

It’s tempting to call the insurance company immediately.

Don’t.

Instead, take the time to read the denial letter carefully.

Many homeowners skim through the document, become frustrated, and miss important details that could help them challenge the decision later.

What to Look For

Review the letter and highlight:

- Claim number

- Date of loss

- Policy provisions cited

- Specific denial reasons

- Inspection findings

- Coverage exclusions referenced

- Appeal instructions

- Response deadlines

Every sentence matters. Sometimes the denial is based on one specific finding. Other times, multiple reasons are listed. Understanding those reasons helps you build an effective response.

Questions to Ask Yourself

As you review the denial, consider the following:

- Did the adjuster inspect every damaged area?

- Were detached structures evaluated?

- Were photographs included in the report?

- Was interior water damage considered?

- Did the insurer accurately identify the storm date?

- Were local weather records reviewed?

The answers may reveal weaknesses in the original investigation.

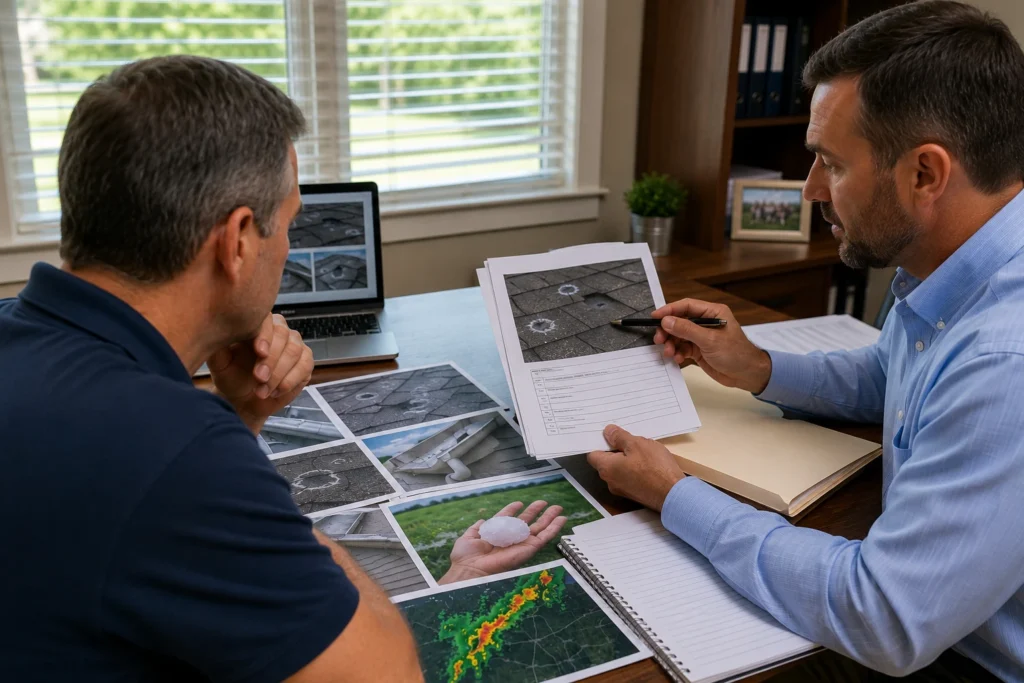

Gather Additional Evidence Immediately

If you’re researching What to Do If Your Hail Claim Was Denied in New Braunfels, TX, one of the most important steps is strengthening your evidence. Evidence changes outcomes. Emotion rarely does. The goal is to create a clear connection between the storm event and the damage present on your property.

Why Documentation Matters

Strong documentation is often what separates successful claim disputes from unsuccessful ones. In many ways, building a persuasive insurance claim resembles the process of creating an evidence-based case where every piece of information supports a larger conclusion. This systematic approach is similar to the concept of Epistemology, the branch of philosophy that examines how knowledge is established and justified. The more reliable and organized your documentation is, the stronger your position may become when challenging a hail claim denial.

How to Document Hail Damage for an Insurance Claim

One of the most important steps after a denial is creating a thorough record of the damage. Proper documentation helps establish the connection between the hailstorm and the property damage being claimed. The stronger your evidence, the easier it becomes to challenge findings that may be incomplete or inaccurate. Detailed photographs, inspection reports, weather records, repair estimates, and organized communication logs can all play a valuable role in supporting your position.

Document Every Area of Damage

Take photographs of every affected area. Don’t assume the roof is the only place where evidence exists.

Capture images of:

- Roof surfaces

- Shingles

- Gutters

- Downspouts

- Siding

- Garage doors

- Window screens

- HVAC equipment

- Fencing

- Outdoor structures

Take both close-up and wide-angle photographs. Close-ups help show specific impacts. Wide-angle images provide context and show the overall condition of the property.

Don’t Overlook Interior Damage

Many homeowners focus entirely on exterior damage. That can be a mistake. Interior conditions may strengthen the connection between roof damage and resulting water intrusion.

Photograph:

- Ceiling stains

- Water spots

- Peeling paint

- Damaged drywall

- Wet insulation

- Mold growth

These issues may support the argument that storm-related damage has affected the home’s interior.

Create a Damage Inventory

Organization matters.

Create a written list identifying:

| Area | Damage Observed |

| Roof | Impact marks and granule loss |

| Gutters | Dents and deformation |

| Fence | Splintering and impact damage |

| HVAC Unit | Fin damage |

| Interior Ceiling | Water staining |

A structured inventory makes it easier to communicate with contractors, adjusters, and other professionals.

Obtain Independent Inspections

A second opinion can be incredibly valuable. Many denied claims involve disagreements about what the adjuster observed during the inspection. Independent inspections often reveal damage that was missed or underestimated.

Roofing Contractor Evaluations

An experienced roofing contractor may identify:

- Hail impact bruising

- Fractured shingles

- Granule displacement

- Damaged flashing

- Compromised vents

- Hidden roof vulnerabilities

Request a detailed written report whenever possible. General comments carry less weight than documented findings supported by photographs.

Engineering Assessments

Some situations justify bringing in a licensed engineer.

Engineering evaluations may help assess:

- Structural concerns

- Material performance

- Storm causation

- Long-term roof integrity

While not every claim requires engineering analysis, it can be particularly useful in larger or more complex disputes.

Drone Photography and Advanced Imaging

Technology has changed the inspection process.

Drone photography can provide:

- Comprehensive roof views

- High-resolution imagery

- Documentation of difficult-to-access areas

- Better visual evidence for negotiations

In many cases, aerial imagery helps support findings that may not be obvious from ground-level inspections.

Collect Weather Data Supporting Your Claim

Weather data can become one of the strongest pieces of supporting evidence. Insurance companies occasionally dispute the severity of a storm or question whether hail occurred at all. Objective weather records can help address those arguments.

Valuable Weather Documentation

Look for:

- National Weather Service reports

- Hail size records

- Storm path information

- Radar imagery

- Severe weather warnings

- Local weather archives

These records can help establish that a hail-producing storm affected your area during the claimed loss period.

Why Timing Matters

The closer your weather evidence aligns with the reported date of loss, the stronger it becomes. If your insurer argues the damage occurred months before the reported storm, weather data may help narrow the timeline and support your position.

Keep Detailed Records of Every Communication

This step is often overlooked. It shouldn’t be. From this point forward, document every interaction related to the claim.

Maintain records of:

- Phone calls

- Emails

- Text messages

- Inspection appointments

- Contractor meetings

- Letters received

Keep a dedicated folder for everything associated with the dispute.

You may never need all of it.

But if the disagreement escalates, you’ll be glad you preserved it.

Prepare for the Next Step

At this stage, you should have:

- Reviewed the denial letter

- Identified the insurer’s reasons

- Documented visible damage

- Collected photographs

- Obtained independent inspections

- Gathered weather data

- Organized communication records

Now you’re in a much stronger position than when the denial first arrived. The next step is presenting that evidence effectively and requesting a formal reconsideration of the claim.

Request a Formal Claim Reconsideration

Once you’ve gathered stronger evidence, it’s time to ask the insurance company to take another look. Many homeowners skip this step and immediately assume they need legal action or regulatory intervention. In reality, claim reconsideration is often the fastest and most cost-effective way to challenge a denial. A reconsideration request allows you to present new information that may not have been available during the original investigation.

When Reconsideration Makes Sense

You should consider requesting reconsideration if:

- New damage has been identified

- Additional inspections were completed

- Weather evidence supports your claim

- The insurer overlooked part of the property

- Independent experts disagree with the original findings

- Repair estimates reveal a larger scope of damage

The stronger your supporting evidence, the stronger your reconsideration request becomes.

Building an Effective Reconsideration Package

Organization matters. A well-organized package is easier for reviewers to understand and evaluate.

Include:

- A written summary of the dispute

- The denial letter

- Inspection reports

- Contractor evaluations

- Engineering reports (if available)

- Photographs

- Weather records

- Repair estimates

- Communication history

Avoid overwhelming the reviewer with unnecessary information. Focus on evidence that directly addresses the reasons for denial.

Address Every Denial Reason Individually

If the denial letter cites three separate reasons, respond to all three.

For example:

| Denial Reason | Evidence to Address It |

| Wear and tear | Independent inspection report |

| No hail event | Weather records and radar data |

| Damage below deductible | Detailed repair estimate |

Leaving one issue unanswered can weaken your position. The goal is to eliminate uncertainty.

Understanding the Texas Appraisal Process

When researching What to Do If Your Hail Claim Was Denied in New Braunfels, TX, you’ll often encounter discussions about appraisal. Appraisal is a dispute-resolution process included in many property insurance policies. However, it’s important to understand what appraisal can and cannot accomplish.

What Appraisal Is Designed to Resolve

Appraisal is generally intended to resolve disagreements involving:

- Scope of repairs

- Cost of repairs

- Property valuation

- Amount of loss

For example, your contractor may estimate repairs at $45,000 while the insurer estimates $18,000. Appraisal may help resolve that difference.

What Appraisal Usually Does Not Resolve

Certain disputes involve coverage rather than valuation.

Examples include:

- Whether damage is covered at all

- Policy exclusions

- Fraud allegations

- Interpretation of policy language

These issues may require different approaches.

Benefits of Appraisal

Potential advantages include:

- Faster resolution than litigation

- Independent review process

- Reduced conflict

- Potentially lower costs

However, every situation is unique. Before invoking appraisal, make sure you understand your policy language and the nature of the dispute.

When a Public Adjuster Can Help

Some hail claims become highly complex. Multiple inspections. Conflicting reports. Large repair estimates. Repeated denials. At that point, professional assistance may be worth considering.

What a Public Adjuster Does

A public adjuster works exclusively for the policyholder.

Their role often includes:

- Evaluating damages

- Reviewing policy provisions

- Preparing estimates

- Organizing documentation

- Negotiating with insurers

Unlike company adjusters, public adjusters are not employed by the insurance carrier. Their focus is representing the homeowner.

Public Adjuster vs. Insurance Company Adjuster

| Public Adjuster | Insurance Company Adjuster |

| Represents policyholder | Represents insurer |

| Advocates for claim recovery | Evaluates claim on insurer’s behalf |

| Independent assessment | Company-directed investigation |

| Assists with negotiations | Handles claim administration |

Understanding this distinction is important. Many homeowners mistakenly believe the insurance adjuster is their advocate. In reality, the insurance adjuster’s responsibility is to evaluate the claim for the carrier.

Signs You May Benefit From Professional Assistance

You may want additional help if:

- The claim involves significant damage

- Multiple structures were affected

- The insurer repeatedly denies coverage

- Estimates vary dramatically

- Policy language is difficult to interpret

- You feel overwhelmed by the process

The larger the claim, the more important proper documentation and negotiation often become.

Why Local Experience Matters in New Braunfels

Every region presents unique challenges. New Braunfels is no exception. The area regularly experiences severe weather, including hailstorms capable of causing significant roof damage. A professional familiar with local conditions understands how those storms affect residential properties.

Local Knowledge Can Make a Difference

Factors that may influence claims include:

- Regional weather patterns

- Common roofing materials

- Local labor costs

- Building code requirements

- Contractor availability

Someone familiar with New Braunfels may recognize issues that an outside reviewer could overlook.

Post-Storm Claim Volume

Following a major hail event, insurance carriers often receive thousands of claims. That surge can create challenges such as:

- Inspection delays

- Scheduling backlogs

- Contractor shortages

- Longer claim processing times

Homeowners who stay organized and proactive often place themselves in a stronger position.

Filing a Complaint With Texas Regulators

Sometimes homeowners believe their claim was not handled fairly. If that occurs, filing a complaint may be appropriate. A complaint does not guarantee payment. However, it may trigger additional review of the claim-handling process.

Situations That May Warrant a Complaint

Examples include:

- Excessive communication delays

- Failure to investigate properly

- Unclear claim decisions

- Unexplained denials

- Concerns about claim-handling practices

The focus should remain on documented facts rather than emotion.

Information You’ll Want to Gather

Before filing a complaint, organize:

- Policy documents

- Denial letter

- Inspection reports

- Photographs

- Correspondence records

- Repair estimates

- Weather documentation

The stronger your documentation, the easier it becomes to explain your concerns.

Protecting Your Rights Throughout the Process

One of the most important lessons homeowners learn is that organization matters. A lot. Insurance claim disputes often involve months of communication, inspections, and document exchanges. Without good records, important information can be lost.

Create a Claim Timeline

Build a chronological record that includes:

| Event | Date |

| Storm occurrence | Record date |

| Initial inspection | Record date |

| Claim filed | Record date |

| Denial received | Record date |

| Follow-up actions | Record date |

A timeline creates clarity and can help support your position later.

Save Everything

Keep copies of:

- Emails

- Letters

- Inspection reports

- Estimates

- Invoices

- Photographs

- Weather records

Digital backups are highly recommended. The more organized your file becomes, the easier it is to respond to questions or disputes.

Avoid These Common Mistakes

Many homeowners unintentionally weaken their own claims.

Avoid:

- Throwing away damaged materials

- Delaying inspections

- Missing deadlines

- Failing to document conversations

- Assuming the denial is final

- Making permanent repairs before documentation is complete

Small mistakes can create larger problems later. What Happens If the Denial Stands? Even after submitting additional evidence, some claims remain disputed. That doesn’t necessarily mean you have exhausted every option.

Possible Next Steps

Depending on the circumstances, options may include:

- Additional inspections

- Supplemental claims

- Appraisal

- Professional representation

- Regulatory complaints

The appropriate path depends on the specific facts involved. No two hail claims are identical.

Evaluating Whether Further Action Makes Sense

Consider factors such as:

- Estimated repair costs

- Strength of supporting evidence

- Complexity of the dispute

- Potential recovery amount

- Time investment required

Sometimes pursuing additional review is worthwhile. Other times, the evidence may simply not support a different outcome. An objective assessment is important.

Why Some Denied Hail Claims Are Later Approved

Many homeowners are surprised to learn that denied claims are sometimes reversed. Why? Because additional evidence changes the conversation. The insurer’s initial decision is based on the information available at that moment. When stronger evidence emerges, outcomes can change.

Common reasons for successful challenges include:

- Better documentation

- More thorough inspections

- Additional weather evidence

- Detailed repair estimates

- Expert evaluations

- Identification of overlooked damage

Persistence, combined with solid evidence, often produces better results than frustration alone.

Final Thoughts

If you’re searching for What to Do If Your Hail Claim Was Denied in New Braunfels, TX, remember that a denial letter is not always the end of the road. Many claim disputes can be addressed through stronger documentation, independent inspections, weather evidence, and organized communication. The key is responding strategically rather than emotionally. Start by understanding exactly why the claim was denied. Gather supporting evidence. Document every damaged area. Obtain independent opinions when necessary. Keep detailed records of every interaction. And if the situation becomes too complex, don’t hesitate to seek professional guidance.

Most importantly, act promptly. Time can affect evidence, inspections, and available options. The sooner you begin building your case, the better positioned you may be to challenge the denial effectively. A denied claim can feel discouraging. However, homeowners who stay informed, organized, and persistent often discover they still have meaningful opportunities to pursue a fair review of their hail damage claim.

FAQs

Yes. Many homeowners successfully challenge denied hail claims by providing additional evidence, inspections, and documentation.

The timeframe depends on your policy and circumstances, so review your denial letter and policy documents as soon as possible.

Insurance companies often deny claims by attributing damage to wear and tear, aging materials, or pre-existing conditions rather than hail.

Yes. An independent inspection may identify damage that was overlooked or interpreted differently during the original evaluation.

Absolutely. Weather records can help establish that a hail-producing storm occurred in your area on the reported date of loss.

Obtain an independent assessment to determine whether the damage affects the roof’s performance, lifespan, or ability to prevent water intrusion.

Appraisal is a dispute-resolution method that may help resolve disagreements regarding repair costs or the amount of damage.

Consider contacting a public adjuster if the claim is complex, involves significant damage, or remains disputed after multiple inspections.

Yes. Homeowners who believe their claim was handled improperly may file a complaint with the appropriate Texas regulatory agency.

No. Many denied claims are later reconsidered when additional evidence, expert opinions, or documentation are presented.